|

FEC

LegacyChange by Insured Grace Contract Simplified Estate Asset Plans LegacyChange.com Home Save Tax Insured-Economical-Efficient Flexible Asset Transfer Through a Non-Profit Asset Transfer Organization |

|

|

Return to LegacyChange Special Beneficiaries Income Plan Asset Transfer - Non-Tax Burden - Gifting Legacy - Plan Privacy &

Guaranteed Inheritance or Divorce Settlement Funds from Real Estate & Assets with Tax savings. Ask us how!

A LegacyChange Plan reduces tax while transferring assets in to a managed & guaranteed insured income flow.

&

&

&

&

& The Family Farm, Ranch & Other Business Legacies to Turmoil &

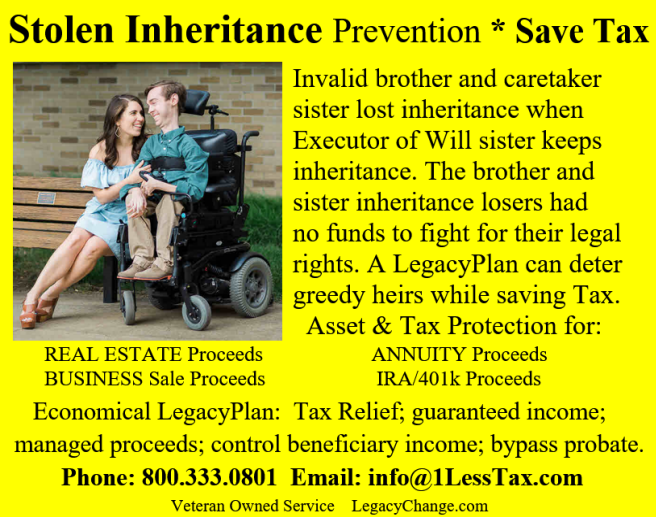

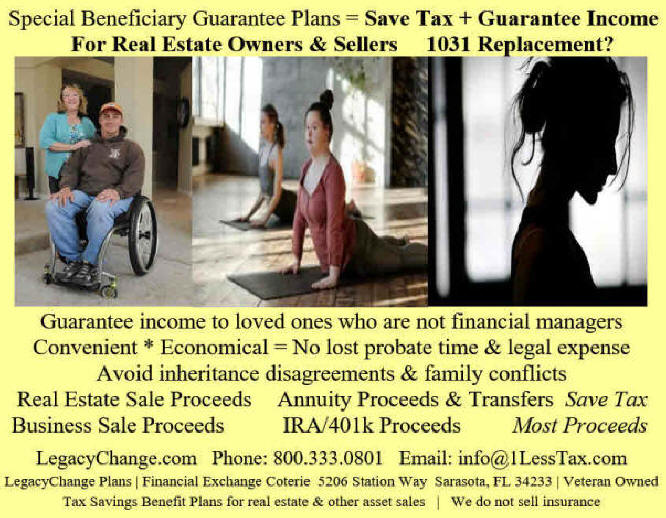

19 Recommendations for Minimizing Inheritance Conflict You worked hard to build your nest egg. You saved, invested wisely and were careful to manage the myriad of risks that threatened your life’s savings. Having invested so much time, effort and sacrifice into getting where you are, it only makes sense that you would like to pass your life’s work on to your loved ones with the least amount of tax and government interference. There are well-established tools to ensure that your financial legacy reaches the intended recipients. Wills, revocable trusts, irrevocable trusts, family limited partnerships (and LLCs), private foundations, and an alphabet soup of strategies—like GRITs, GRATs, CRUTs, CRTs, and QPRTs, to name a few—make estate transition efficient and tax free for all but the truly wealthy, and therefore are an indispensable part of a secure financial plan. Your Most Valuable Asset But this article is not about current estate-planning strategies. Although an important subject, and one that occupies the estate planning community and the clients we serve, I want to talk about your most valuable and enduring asset, the asset that for better or worse survives you and impacts generations to come: family. Family is truly the gift that keeps on giving. The family dynamic that you had a hand in creating will survive you, impacting your children and grandchildren. Although many of the events that went into forming your family as it now exists have already occurred, your family is not set in stone. How you live your life from this point forward and how you structure your estate at death are new opportunities to reinforce the healthy aspects of your family, correct past wrongs, and leave a lasting legacy of fairness, compassion and love. Family survives long after an inheritance is either spent or is tucked away in the accounts of our beneficiaries. Despite our greatest efforts, wealth comes and goes. Even great wealth is often gone in a generation or two. History is replete with stories of successful entrepreneurs who amassed fortunes only to have them wasted within one or two generations after their death. T In addition to the transmission of wealth, our estate plan communicates many things to those we leave behind. We say who is remembered, who is loved, who is important, who we trust and who we trust to be in charge. It carries additional weight, because it is our final statement. Unlike fights or misunderstandings during life, we cannot take back or fix the insensitivities, oversights or hurtful provisions of our estate plan. The greatest slight is to not plan at all. By failing to plan, we communicate our apathy and the message that our loved ones were not worthy of being remembered. With so much at stake, we owe the process as much attention and thought as we can muster. Anticipating and Avoiding Conflict It is especially important to anticipate conflict. Inheritance conflict is often the final straw for challenged families, with members vowing to never speak to one another again. Special circumstances require special planning. If you have re-married, you must balance the financial and emotional needs of your spouse with those of your natural children. If your children don’t get along, then you must choose fiduciaries carefully. Other unique factors require special attention, like a family business, a family cottage, or a handicapped or addicted child. Ideally, as the parent, you should lead in the prevention effort. You are in the best position to create family peace and minimize future fighting. Use your position, perhaps as you never have, to build bridges and mend fences. You may not ultimately be able to undo the old hurts that brought the family to its current state, but you must never stop trying. You can best lead by having your estate affairs in order. Similar to succession planning in business, you need a transition plan and a transition team to implement your vision. Now is the time to take stock of your family portfolio. As the family CEO, you can implement a plan and secure the future course for your family and your assets. The stepparent-stepchild relationship is particularly fraught with problems, as both vie for the love and affection of the natural parent. Children have difficulty understanding that their natural parent is, or was, a person with real needs that the stepparent fulfills or at one time fulfilled. Children must also understand that the stepparent has legitimate concerns about his or her economic well-being after the death of their spouse. Stepparents, in turn, must understand that children see their parent’s inheritance as the final statement of love and that the stepparent is perceived as interfering with that connection. Finally, the natural parent in a second marriage must be sensitive to the personal dynamic between his children and the new spouse and take every step possible to keep the peace between both camps during life and after death. Actions That Can Reduce Conflict Exceot for a Legacy Plan there is no single cure that will prevent inheritance disputes. Instead, prevention requires a multi-faceted approach that combines psychology, a Legacy Plan, a lot of self-awareness and a good dose of common sense. The following 18 recommendations are aimed at minimizing inheritance conflict: 1. Address personal property separately Leave a separate list of cherished personal property with instructions as to who should inherit each item. Personal property is often a source of conflict among family members. Most states admit a separate personal property list (sometimes called a Personal Property Memorandum) as part of the will. A separate list can be handwritten or typed but must be signed and dated. Each state with property must be addressed. The list should be of sufficient detail to effectively describe each item being gifted. 2. Update estate plan regularly Make estate planning changes when there has been a change of circumstances, especially after a divorce. Although most states’ matrimonial laws nullify beneficiary designations and will provisions that favor former spouses, it is unclear whether a former spouse continues to be empowered under medical or financial powers of attorney. To avoid unwanted and bizarre results, former spouses should be immediately disinherited and stripped of all powers. Additionally, estate planning should be reviewed after other life changes, like the death or divorce of a child or the illness, addiction or incapacitation of any beneficiary. 3. Hold an open discussion on special assets There are situations where family input is advisable. Issues like care for a handicapped child, succession of a family business, or continued enjoyment of a vacation home require parents and children to be on the same page. 4. Consider a prenuptial agreement Second marriages are one of the most significant indicators of inheritance conflict. A prenuptial or a post-nuptial agreement will minimize conflict at death by clearly stating the relative entitlements of spouses and other beneficiaries, such as children not of the marriage. 5. Clearly identify gifts and loans Parents often help adult children who are experiencing financial distress. It is the parent’s prerogative to structure such advances as either loans or gifts. Unpaid loans from mom and dad can be a source of conflict, activating jealousies about who got more. Parents should resolve uncertainty regarding lifetime advances by addressing them in their estate plan. 6. Properly fund trusts and Legacy Plans If a trust is performed in lieu or in addition to a Legacy Plan, all assets should appropriately re-titled into a trust to avoid probate and confusion as to the testator’s intent. For example, if the will or trust leaves equally among the testator’s children, all life insurance policies and annuities could name the trust as beneficiary. This can be more simply and expediently performed by addressing beneficiary amounts assigned in the Legacy Plan or insurance beneficiary documents. Non-qualified annuity transfers are taxed at ordinary income tax rates. A Legacy Plan can reduce much tax burden from Annuity transfers. 7. Avoid joint ownership Joint ownership (i.e., placing a child’s name as a joint owner of a parent’s asset) is an inefficient method to pass assets at death and can produce unintended results. Adding a beneficiary as an owner of assets like real estate confers significant and sometimes irrevocable lifetime rights, which expose the donor to the co-owner’s liabilities and limits the donor’s ability to change his or her mind in the future. The most efficient and predictable plan is to fund all assets into a trust. 8. Pre-arrange funeral details Making funeral arrangements and choosing the form of interment in advance can avoid conflict and the strong emotions that such decisions sometimes elicit. For example, re-married widows and widowers should determine in advance who is to be buried with whom. Pre-planned and detailed written funeral instructions avoid controversy and angst. 9. Name spouse as primary fiduciary Absent special circumstances, one’s spouse in a first marriage should be named as primary and sole fiduciary. As recently as the 1970s, well-heeled husbands, even in first marriages, commonly named bank and trust companies as trustee of trusts established for their wife and children. Today, such arrangements would be unacceptable to most wives, as women have become full participants in the family economic unit. In second marriages where there are children not of the marriage, each spouse should consider establishing his or her own separate revocable trust. While each spouse may act as the other’s fiduciary, it may be preferable to appoint a neutral third party or professional (corporate) trustee to mediate the disparate interests of the surviving spouse and natural children. It is not advisable to name a spouse as co-fiduciary with children not of the marriage. Stepparents and stepchildren are natural competitors and in most cases should not be forced to work together. 10. Make logically defensible choices Determining who is “in charge” is an emotionally loaded issue. It is perceived as the testator’s statement as to who is the most competent and trustworthy. Such decisions are reminiscent of the day when mom went to the store and put one of the children, usually the oldest, in charge. Mom hadn’t left the driveway before younger children would protest: “You’re not the boss of me,” or more prophetically, “Who died and left you in charge?” Appointing fiduciaries can be seen as an act of favoritism and should be thoughtfully considered. Naturally you want the best person for the job to ensure that your wishes are properly carried out. However, parents must still be sensitive to their children’s emotional reactions. Children can rationalize an older sibling being appointed simply on the basis of seniority. They can also accept the naming of in-towners over out-of-towners on the basis of convenience and geographic desirability. Children, however, cannot accept appointments that disturb the traditional family hierarchy and pecking order. Where children are equally situated, appoint them as co-fiduciaries. Don’t leave anybody out; name a younger or less-able child as successor to a successor if for no other reason than to show that you remembered them. 11. Be aware of long-established sibling roles In addition to age, name children on the basis of traditional family leadership roles. It is an insult in the order of disinheritance to take a leadership role away from a deserving child who has traditionally held that role and served it well. 12. Appoint a committee Naming a committee of fiduciaries has a number of benefits: Two heads are better than one; a committee keeps each member honest; communication with non-fiduciary beneficiaries is facilitated by having more than one spokesperson; and multiple fiduciaries can share the work load and minimize burnout and resentment. Misunderstandings can quickly escalate when a single overburdened fiduciary fails to respond to beneficiary inquiries in a timely manner. In turn, a single fiduciary may resent repeated inquiries from what they perceive as greedy or overly-eager beneficiaries. The failure of an overburdened fiduciary to respond to inquiries in a timely manner raises suspicions that the fiduciary is trying to hide something. A committee solves many of these problems and should be considered, as long as all of the members of the committee get along. 13. Recognize primary obligation when in first marriage Except where extenuating circumstances dictate, in first marriages one’s surviving spouse should be named primary and sole beneficiary. A testator’s first obligation is to his or her surviving spouse. As children can no longer be expected to care for ill or aging parents, spouses must leave each other in the best possible position to provide for their own needs. The risk that children will be disinherited is minimal, as they are the logical beneficiary of both spouses. 14. Balance the needs of second spouses and children Care should be taken to accommodate the financial and emotional needs of both the surviving spouse and children. Consider an outright transfer to natural children at the death of the first spouse of an amount that will not jeopardize the well-being of the surviving spouse. Parents who completely withhold all distributions to their children until after the death of a stepparent create a potential deathwatch. There is no impatience like that of a stepchild waiting for their stepparent to die in order that they may receive what they believe to be rightfully theirs. 15. Leave to children equally and disinherit only as a matter of last resort Treat children equally. An unequal allocation is a blatant and unforgivable showing of favoritism that will re-activate old sibling rivalries and hurt feelings. Children have unequal needs growing up. Some will naturally receive more based on special skills (travel sports, private schools, piano lessons), or special needs (braces, glasses, special shoes, or furlough from physical labor). However, the past is the past; don’t be tempted to leave unequally at death to account for early inequities. Don’t penalize successful children by leaving more to their needy siblings, or conversely, reward successful children because they are favored. Exceptions to this general rule are the truly handicapped and those who would use their inheritance to further an unhealthy lifestyle of addiction or sloth. Finally, be certain before you disinherit, as it leaves a lasting legacy of hurt and rejection. It is your decision. A Legacy Plan can be specific and ersonally care for each beneficiary. 16. Make lifetime gifts Attempt to accommodate special needs through lifetime gifts as a Legacy Plan. A Legacy Plan can be a Lifetime gift, like a dowry for a daughter or a stake for a son, have been used throughout history to accomplish inheritance objectives. Children have extremely sensitive antennae for detecting favoritism and could become aware of such gifts. A Legacy Plan is generally appreciatedc and accepted by beneficiaries. 17. Transition family business A family business could pass to those family members who have been active in the business and who are instrumental to its future success. The fragile nature of businesses requires that there be a smooth transition from one generation to the next. Less business connected beneficiaries could be comfortable with a Legacy Plan. A seamless transition requires the gradual pass of the torch while parents are alive. Parents should groom their successors by gradually transferring responsibility and authority to their successors over time. Non-business assets can be used to equalize the share for children not active in the business. Life insurance can be used to augment the value of the estate to ensure that sufficient assets are available to achieve an equal distribution to all children. 18. Keep estate planning content private Clients often ask whether they should give a copy of their estate plan to their children. With the exception of health care powers of attorney (living wills), the answer for most families is “no.” One can inform and discuss, but the client should maintain control and client wishes. As in the movie “Back to the Future,” you don’t want knowledge of the future to affect the course of history. As author, you reserve the right to change the ending of your personal history. Giving documents during life creates the expectation that no changes will be made. Later changes will be viewed as taking away something previously given. We don’t know the future; keep open the possibility that things may change. The Legacy Plan has much of this ability for future adjustments. 19. Use a LegacyChange Legacy Plan or Plans to avoid conflicts and family discourse. Conclusion Many of the problems of inheritance are themselves inherited. They are both genetic and acquired, but they are not inevitable. Inheritance disputes can be explained and predicted and are to a large degree preventable. By carefully and thoughtfully planning your estate, you can protect your most important legacy and prevent conflicts with a Legacy Plan. & When it comes to having a family-run farm operation remain that way, succession planning can be an uncomfortable, sensitive, but at the same time necessary step. People can’t, or don’t want to run the farms forever and having a plan in place focusing on how to move forward once the time comes can make things a little easier during transition periods. One of, if not the most important element of succession planning is communication. Communicating the intentions, timeline, questions and concerns will help keep the transition period transparent and allow for everyone involved to be on the same page. Here are some things to consider when succession planning is on the horizon. Start early, involve everyone and reviewBeginning the succession planning process early allows for more time to consider every element of the plan itself. The plan may not come into effect for an extended period of time, but it doesn’t hurt to be prepared. By including everyone involved with the farm in the process, it allows for more avenues of communication and for roles to be defined. Some people may not want to be involved with the farm, whereas others want to be heavily involved in the daily operations. Bringing everyone to the table can make it easier to decide where people stand on the succession plan and the future of the farm. Reviewing the succession plan on a regular basis can allow for the plan to be fresh in the minds of those involved. In the event of someone changing their minds and wanting a different part in the plan, the issues can be tackled in a timely manner and the succession plan can move forward. Identify successor(s), goals and objectivesThroughout the succession planning process, someone should be chosen or volunteer to be the successor of the farm. Without goals and objectives in mind, the succession plan may not be very viable. Coming up with a list of them can help the succession plan get off the ground and gain momentum. Some objectives can include meeting a certain profit margin, introducing new crops or equipment and deciding to sell or lease some of the land. A revocable trust, or for some tax situations, an irrevocable trust, is a must considertation to avoid probate, maintain privacy, avoid months in court and avoid 1%-3% of estate expense for probate attorney fees. A Legacy Plan could solve disputes and assist those who are challenged to care for financial responsibility. The current tax advantage with a step up tax exclusion at death is a primary consideration. & LegacyPlan Transaction Worksheet for Illustration (pdf) &

&

Return to LegacyChange Go to Incentive Plan |